|

||||||

| Home Nation World Business Opinion Lifestyle China Focus ChinAfrica Video Multimedia Columnists Documents Special Reports |

|

||||||

| Home Nation World Business Opinion Lifestyle China Focus ChinAfrica Video Multimedia Columnists Documents Special Reports |

| 2017 in Retrospect > Top 10 Business News Stories |

| Dawn of Cashless Societies |

| Fintech companies want to enable payment without cash or credit worldwide |

| By Bryan Michael Galvan · 2017-07-28 · Source: | NO. 31 AUGUST 3, 2017 |

People walk past a store where Alipay is available in Kuala Lumpur, Malaysia, on May 22 (XINHUA)

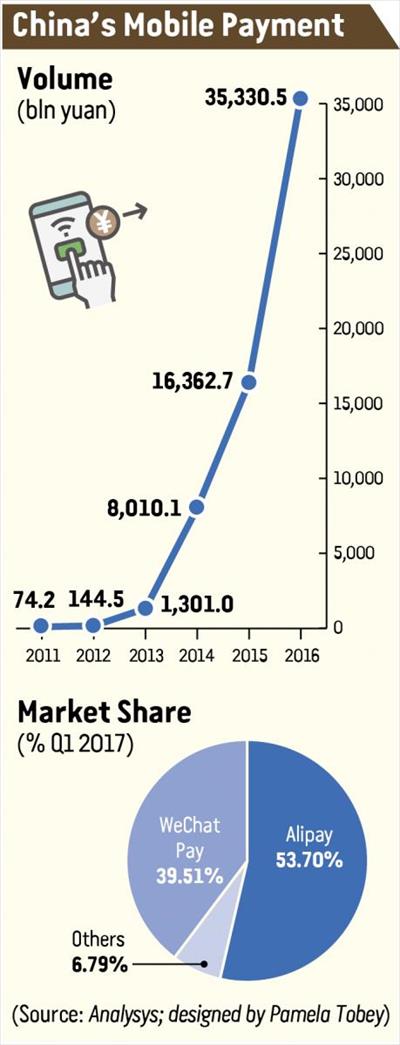

China's mobile payment providers are working to kickstart cashless societies around the world. Riding on the back of the growing numbers of Chinese tourists abroad, companies such as Ant Financial Services Group's Alipay and Tencent's WeChat Pay are developing new ways for consumers to spend their money while traveling without having to carry cash or credit. In doing so, these enterprises seek to gain a foothold in countries that lack traditional credit card infrastructure, and grab hold of a nascent market that may fundamentally change how people interact with money. In China, electronic wallets are ubiquitous, used for transactions both small and large. Last year, Chinese consumers made 35.3 trillion yuan ($5.2 trillion) worth of payments via mobile devices—around half the nation's GDP, according to Internet consulting firm Analysys. By linking their bank accounts to mobile payment platforms, users can use the e-wallet services on their smartphones to pay rent and utility bills, hail taxis, manage their finances and do more. Due to the increasing use of these platforms, the amount of mobile payments in China is now 50 times greater than that in the U.S.—which amounted to $112 billion in 2016, according to data from American market research company Forrester Research. The services provided by these companies have spread to small merchants and individuals who might not need to use cash or credit cards at all due to the convenience and ease of mobile payment options and the limited number of point of sale terminals in stores.

A customer uses Alipay to pay at a food market in Rome, Italy, on April 7 (XINHUA)

Eyeing outside markets Chinese financial technology (fintech) companies aiming to expand their operations outside China by taking a cut from tourism spending have taken note. Chinese tourists spent $261 billion during their travels abroad last year, 12 percent more than the previous year, and the number of outbound travelers grew 6 percent to 135 million in 2016, according to figures from the United Nations World Tourism Organization (UNWTO). "This growth consolidates China's position as the number one source market in the world since 2012, following a trend of double-digit growth in tourism expenditure every year since 2004," the UNWTO report said. "The growth in outbound travel from China benefited many destinations in Asia and the Pacific, most notably Japan, [South] Korea and Thailand, but also long-haul destinations such as the United States and several in Europe." Despite having the world's leading outbound market, the number of ordinary Chinese passports in circulation was 120 million in October 2016—an estimated 8.7 percent of the population, based on figures by the Ministry of Public Security. Compared to the United States' passport possession rate of approximately 39 percent of the population in 2015, China's tourism market has ample room to grow. A recent survey by Counter Intelligence research group reports that Chinese air travel to Europe increased by almost 20 percent in 2016, with travelers predicted to hit 90 million by 2025. In January, Ant Financial and U.S. money transfer company MoneyGram announced a merger which would give the former access to 350,000 physical locations and 2.4 billion bank and mobile accounts under MoneyGram. Nonetheless, there are numerous obstacles in the way of mass adoption of mobile payment, including fragmented reception among merchants—in part due to the growing variety of options available to consumers. Beijing-based QF Pay seeks to provide a one-stop mobile payment solution to merchants that would enable them to accept payment from customers that use a variety of mobile wallets and payment methods. Patrick Ngan, President and Co-Founder of global mobile payment technology solutions provider QF Pay, told Beijing Review that Southeast Asian countries all want to attract Chinese money. "Merchants all want Chinese tourism money. Those big conglomerates, those big shopping malls, they all want to have a big sign saying 'we welcome you' in Chinese because they know [the tourists] spend big." Chinese mobile payment firms will also butt heads with conventional payment leaders such as Visa and MasterCard. "If you look at the [history and cycle of] payment methods, from bartering to gold to cash and card... what's next? Mobile payment. The ability to make purchases via their mobile phones anywhere, anytime, both online and offline, will be highly disruptive to the entire payment landscape. It will change both consumer behavior and the way retailers conduct their business. They want to disrupt the entire credit card market. I'd be very worried if I were the credit card providers. But then I look at this as very healthy competition," said Ngan. "If the sector doesn't have competition, then you'd be worried. There is going to be consolidation along the way, but mobile payment is only scratching the surface at the moment."

A customer uses WeChat Pay to shop at a convenience store in Bangkok, Thailand, on May 5 (XINHUA)

Dealing with differences In China, mobile payment gained momentum following the use of social media apps like WeChat to send hongbaos—red envelopes with money—during the Chinese Spring Festival. Sending hongbaos was already a common practice, so once it became digitalized, the custom spread to sending e-gifts to friends and family in a complimentary fashion. While that approach worked in China, the concept may not carry over to other countries unfamiliar with it. Chinese mobile payment companies will need to deal with different economic and cultural environments overseas. A spokesperson from Ant Financial told Beijing Review that they're addressing the challenge by working together with local partners. "Different markets have different environments and different growth paths for online and mobile payments. For instance, Alipay was created as an escrow service to facilitate online purchases back in 2004. In some of the markets where Ant Financial has local partners, e-commerce is not as prevalent as in China where mobile payment has started flourishing. The key for us is to rely on our local partners, who have deep understanding of local environment and user behavior," said the spokesperson from Ant Financial. The Internet and Mobile Association of India claimed that the number of mobile Internet users in India was expected to reach 420 million by June. The report stated that rural India's mobile Internet penetration would grow at a higher rate than that of urban areas. Now, Prime Minister Narendra Modi's plan to demonetize and reduce India's reliance on cash may come as a windfall to mobile payment firms like Paytm, Ant Financial's local partner in India. One of the reasons why mobile payment proliferated in China was due to the lack of credit card infrastructure in the past which allowed companies such as WeChat and Alipay to leapfrog technological hurdles. Fintech firms are growing in tandem with the number of rural consumers connecting to mobile Internet. "A cashless lifestyle is not just about payment. It allows people to access basic financial services like saving, credit and financing in a low-cost and inclusive manner," said the spokesperson, adding that the company wants to build a system where people's purchases and transactions can contribute to their credit history. After accumulating payment history records, Ant Financial aims to provide micro loans for individuals as well as small businesses. "In inland provinces, a higher percentage of Alipay transactions are conducted on mobile devices, compared with coastland areas. People in rural areas who didn't have easy access to traditional financial services rely more on digital and mobile," said the spokesperson. But while this strategy may work in countries such as China and India, fintech firms must tackle ingrained consumer habits in Western countries that are dominated by legacy payment methods. Mobile payment firms are addressing this challenge by tailoring products to merchants, analyzing big data from consumers and loyalty programs. The mobile payment eco-system in China is highly developed to the point where one doesn't need to carry physical cash in their pockets anymore. As long as their mobile phones still have power, people can make purchases almost anywhere, anytime. However, China's neighboring countries, particularly Southeast Asia, are still at what Ngan calls the Mobile Payment 1.0 Stage.

"There are plenty of mobile wallets out in the market, but not many merchants are being linked up with mobile payment systems that can accept payment from mobile wallets. It takes two to tango, in mobile payment terms, merchants and consumers will need to be linked up at each end with mobile payment systems in order to facilitate payment execution. Everyone is trying to fight for that space, swiping a card and getting a cut out of it. But what is next after that? This is what QF Pay has. We're what you call Mobile Payment 2.0." Ngan said that the company is capable of analyzing data collected from mobile payment transactions and using the information to provide merchants with digital marketing solutions such as e-promotions, e-marketing and various programs to build customers' loyalty, thus allowing merchants to actively engage their customers. "We are the ones who will provide them with those solutions." He claimed if mobile payment is done smartly, by collecting data and working with merchants to actively engage their customers, there will be a segment of customers who will need the service. "Because of the data collected via mobile payment, restaurant owners will be able to tell which dishes are most popular on their menu. As such, less popular dishes can be changed…Also, because of this information, they will be able to source ingredients for these popular dishes more effectively." While mobile payment companies are spurring the creation of cashless societies, security concerns are on the rise following reports of criminals using fake barcodes and quick response codes to steal personal information and users' money. The Better Than Cash Alliance, a global partnership of governments, companies and international organizations seeking to accelerate the transition from cash to digital payments, told AFP that the authorities, while working out "the right balance between innovation and regulation," have been "more active" in their attempts to reduce financial risk and fraud. Copyedited by Sudeshna Sarkar Comments to zhouxiaoyan@bjreview.com |

| About Us | Contact Us | Advertise with Us | Subscribe |

| Copyright Beijing Review All rights reserved 京ICP备08005356号 京公网安备110102005860号 |