|

Quasi-municipal bonds have soared in recent years. How would you explain the growth and the function of these bonds?

It is true that quasi-municipal bonds have increased in recent years. These bonds benefited the investors and issuers, which is the major cause for its increasing issuing scale.

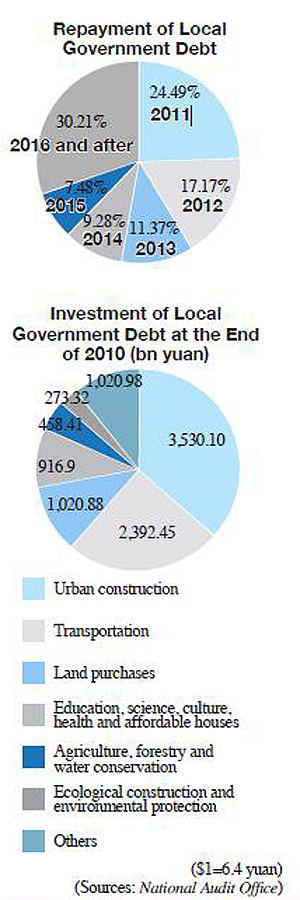

During the 11th Five-Year Plan (2006-10), the issuing of corporate bonds approved by the NDRC totaled 1.297 trillion yuan ($198.59 billion), in which quasi-municipal bonds totaled 347.5 billion yuan ($54.47 billion), accounting for only 26.8 percent of the total.

The issuance of quasi-municipal bonds must meet strict requirements, including the securities law and the regulations on corporate bonds. In addition, it is imperative that capital raised through selling quasi-municipal bonds be used to fund government-backed projects according to the country's industrial policy and other regulations. The capital has been used in building urban sewage systems, roads, bridges, gas and power supply pipelines, affordable houses and municipal rail systems, treating polluted rivers and lakes, and in other infrastructure projects. These projects have helped improve urban facilities, treat pollution and protect the environment, which are beneficial to local social and economic development.

With the further development of the capital market, the quasi-municipal bonds will surely expand. In addition to providing more regulated and transparent funding channels for urban infrastructure construction, the bonds also serve as excellent investment tools with fixed gains for investors.

What can supervisory departments do to better guard against the possible risks from quasi-municipal bonds?

At present, quasi-municipal bonds have been functioning normally regarding repaying capital and interests. But we should not forget the fact that quasi-municipal bonds, as a credit product, are not completely exempt from risks. Investors' worries have reminded us to pay more attention to the potential risks of such bonds and to take measures to protect bond investors' interests.

As the administrative sector monitors the issuing of quasi-municipal bonds, we have kept issuers under close watch. For local government financing vehicles to issue bonds, they must meet basic requirements. For example, local bond issuers must make profits for three consecutive years and the annual average net profit in three years should cover the interests of the bonds issued.

Since last year, we downsized the bond issuers to those top 100 counties with the highest fiscal revenue in China. What's more, we don't let local governments with debts of more than 100 percent of fiscal revenue sell bonds. The strict conditions have kept some unqualified bond issuers out of the market and reduced the scale of quasi-municipal bonds, which also controlled risks. In order to prevent some irresponsible governments from leaving their debt to their successors, we stipulate that the repayment should be divided into different years.

What will be done to improve the systems of administering quasi-municipal bonds?

This problem is not an isolated incident, but a complex one involving systematic perfections.

First, China is still in the process of urbanization and needs to raise funds for its many local infrastructure projects. There's still a big gap between urban and non-urban areas. The fact is that the process of urbanization is far from complete. The important feature of rapid urbanization is huge demand for investment in infrastructure. During this process, raising capital from issuing bonds will be necessary. In this sense, we need to set up a mechanism for regulating local government borrowing to put the risk under control.

Second, bonds via local government financing vehicles remain and will continue to remain an effective financing tool, but they need more improvement. The birth of local government financing vehicles was a result of changes in China's financing system for infrastructure construction. While local governments were barred from directly selling bonds and acquiring bank loans, many local government financing vehicles were created to become the investment and operation bodies for those infrastructure projects. This change introduced the role of the market and made bonds issued by companies set up by local authorities the most transparent among all kinds of borrowing by local government vehicles. In this sense, the bonds via local government financing vehicles still have space for development in the future. Buyers of China's quasi-municipal bonds will not enjoy exemption from interest income tax as their international counterparts, which made the interest rates for issuing quasi-municipal bonds high. The fact is that capital raised through quasi-municipal bonds was used in infrastructure construction which feature a long payoff period and low investment returns. High interest rates actually should not be a part of quasi-municipal bonds. In the future, we will improve the system for bonds via local government financing vehicles and make them real municipal bonds in terms of investment return and payoff period.

Third, the government should set up a monitoring system for local government debt. Many scholars and experts have offered suggestions on how to establish a regulated financing channel for local governments and enhance risk controls and debt administration for local governments. Since China has no unified risk management system for local government debt, the most urgent task is to establish a monitoring system and draw up risk control standards for government debt based on amounts outstanding. Debt with direct or indirect repayment obligations on the part of local governments should be monitored.

|