|

|

|

The building of the People's Bank of China (XINHUA) |

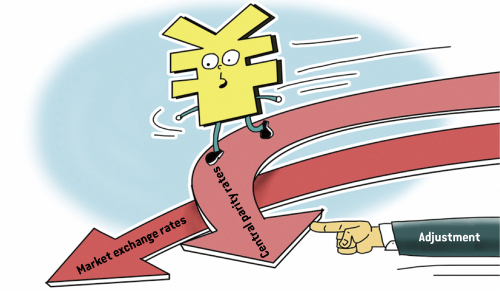

China has changed its central parity system to better reflect market development in the exchange rate between the Chinese yuan against the U.S. dollar. The move is another step toward market forces determining the value of the currency. The yuan fell sharply in value following the decision, raising worldwide concern that volatility will become a drag on global economic growth.

As of August 11, daily central parity quotes reported to the China Foreign Exchange Trade System before the market opens are based on the closing rate of the inter-bank foreign exchange (forex) rate market of the previous day, supply and demand in the market, and price movement of major currencies, the People's Bank of China (PBC), the nation's central bank, said.

So what exactly is the central parity rate? Each trading day at 9:15 a.m. Beijing time, the central parity rates of the yuan are announced against 11 major currencies, including the euro, sterling, U.S. dollar and the Japanese yen. When the inter-bank forex market opens 15 minutes later, trading may only take place within 2 percentage points of the rate.

The PBC cited the large and long-running deviation of the yuan's central parity from its actual market rate as the major reason for the change. This deviation had undermined the authority and the benchmark status of the central parity system.

From government-designated to market-oriented central parity rates, the yuan has taken another step toward its global journey. Although the unexpected policy change triggered dramatic market turbulence, the long-term benefits of the change outweigh the short-term pain.

|

|

A bank clerk counts banknotes in Lianyungang, east China's Jiangsu Province, on August 11 (XINHUA) |

Market reaction

The unexpected move prompted a three-day slump in the yuan. The central parity rate of the yuan against the U.S. dollar weakened by 1,136 basis points, or 1.9 percent, to 6.2298 on August 11. It dipped a further 1,008 basis points, or 1.6 percent, to 6.3306 on August 12. On August 13, the rate further weakened by 704 basis points, or 1.1 percent, to 6.401 against the U.S. dollar, according to the China Foreign Exchange Trading System.

As the yuan tumbled, fears grew in the market that the policy change would spearhead a depreciation trend. To allay such fears, the PBC held a news conference on August 13, reassuring the market that the bank is capable of keeping the exchange rate stable at an adaptive level of equilibrium, and that the yuan will remain strong over the long run.

According to the PBC, the exchange rate tumble was triggered by an attempt to bring the central parity rate closer to the market consensus.

Zhang Xiaohui, Assistant Governor of the PBC, attributed the sharp depreciation to a long-standing gap between the central parity rate and the previous day's closing rate on the inter-bank market. She said the shift was a one-off technical correction and should not be interpreted as an indicator of future depreciation.

"The value of the yuan has gradually returned to market levels as the discrepancy between the central parity rate and the actual trading rate has been largely corrected after declines in the past few days," Zhang told the media." There used to be a 3-percent gap accumulated between a lower official rate and higher market expectations."

She added that there are no grounds for a persistent and substantial depreciation because sound economic fundamentals will determine that the yuan re-enters a period of appreciation.

Zhang saw the country's abundant forex reserves, stable fiscal conditions and healthy financial system as foundations for a strong yuan in the long term.

Following the news conference, the yuan showed signs of improvement in both onshore and offshore markets. On August 14, the central parity rate of the yuan strengthened by 35 basis points to 6.3975 against the U.S. dollar, the first increase since the policy change. The rate stabilized in the following trading week at around 6.4.

Although the Chinese central bank called the new policy a free-market reform, it is seen by some as the start of a long-term depreciation of the yuan to spur China's ailing exports. In July, exports totaled $195 billion, a fall of 8.3 percent year on year.

Yi Gang, Vice Governor of the PBC, dismissed media reports that Chinese authorities had demanded a 10-percent depreciation of the yuan by the end of 2015 in the hope of rescuing the country's sliding exports. He described such reports as "completely baseless."

"China's export conditions are generally stable. Combined with such an enormous trade surplus, it is totally unnecessary for China to adjust the exchange rate to spur exports," Yi said. "Under a managed floating exchange rate system, the value of the yuan is determined by the market."

According to the vice governor, the central bank will no longer regularly intervene in the exchange rate but will continue to manage it, especially when volatility exceeds a tolerable range.

"The system (a managed floating exchange rate system) fits China because it allows for flexibility in the rate and enables effective control of excessive volatility, which boosts market confidence and facilitates a stable economy," Yi said.

Improvement on the forex rate formation system is aimed at building a more effective market-based mechanism, so as to advance future currency reforms, especially the full convertibility of the yuan under the capital account, he added.

Yi Xianrong, a researcher with the Institute of Finance and Banking at the Chinese Academy of Social Sciences, said that currency depreciation would not necessarily improve a country's trade conditions.

"Currency depreciation will lead to cheaper exports but will cause the cost of imports to rise. Therefore, it's likely that the country's foreign trade conditions will be worsened instead of improved," he said.

He dismissed as groundless concerns that a depreciation of the yuan will cause global deflation and that China is exporting its deflationary pressure worldwide.

"What analysts are really concerned about is that a depreciation of the yuan will exacerbate China's economic conditions, reduce China's external demand and fail to lift the global economy out of its difficulties," he said.

|

|

(XINHUA) |

Long-term approach

China's forex reform officially started in July 2005 when the central bank decided to unpeg the yuan against the U.S. dollar and allowed it to fluctuate against a basket of currencies.

The yuan has long been one of the world's strongest currencies. From July 2005 to June 2015, its nominal effective exchange rate appreciated by 46 percent, according to statistics from the Bank for International Settlements.

The International Monetary Fund (IMF) hailed the central bank's latest move as a welcome step that allows market forces to have a greater role in determining the exchange rate. Although the IMF claimed that China's move has no direct implications for the criteria used in determining the composition of the Special Drawing Rights (SDR) currency basket, it said a more market-oriented exchange rate would facilitate SDR operation in case the yuan were included in the basket going forward.

Allocated to IMF members on the basis of their contribution to the fund, SDR represents a reserve that may be drawn upon in times of need. Currently, the SDR basket consists of four currencies--the U.S. dollar, euro, British pound and Japanese yen.

The composition of the SDR basket had been scheduled for a once-in-five-year review this coming November, but the review was postponed to September 30, 2016. Whether or not to add the Chinese currency to the basket is a major issue for the review.

"Greater exchange rate flexibility is important for China as it strives to give market-forces a decisive role in the economy and is rapidly integrating into global financial markets," an IMF spokesperson said on August 12.

The IMF believes an effective floating exchange rate can be established in China within two to three years.

"The reform made the yuan more market-driven, laying a foundation for the free exchange of the yuan," said Liu Weiming, an analyst at China Citic Bank. "It helps clear some of the technical hurdles for the yuan to join the SDR."

After the change in the central parity formation system, how should China press ahead with its forex reform?

Huang Yiping, Deputy Director of the National School of Development at Peking University, said exchange rate reforms during the past decade have had three objectives--letting the market play a bigger role; two-way fluctuation of the yuan exchange rate; and keeping the exchange rate generally stable.

"Future reforms should still follow this direction," Huang said.

"The next big move would probably be further expansion of the exchange rate trading band and more market elements in the central parity rates," Huang said. "Also, more forex products will be created and the opening up of China's forex market will be accelerated."

Zheng Lei, a board member of CMB International Asset Management, warned that exchange rate reform should be carried out with extreme caution.

"China's financial system still has lots of aspects that are not connected to the global market. Against this backdrop, things will get out of control if there is too much haste in forex reform and opening up," Zheng said.

"Although China has roughly a $3.5-trillion forex reserve, it can hardly guard itself against those short-sellers in global institutions. When taking steps to internationalize the yuan, such as getting the currency included in the SDR, consideration should be given to current conditions in China's financial system," Zheng said. "Just because China has a huge amount of forex reserve, it doesn't mean China can act capriciously in forex reform."

Timeline of Reforms on Yuan

August 11, 2015: The People's Bank of China (PBC) adjusts the exchange rate formation system by taking into account of the closing rate on the previous day to better reflect market development.

November 27, 2014: The PBC says it had largely withdrawn from intervention in daily foreign exchange business.

September 30, 2014: China starts direct trading between the yuan and the euro on the inter-bank foreign exchange market.

June 18, 2014: China starts direct trading between the yuan and the British pound on the inter-bank foreign exchange market.

March 18, 2014: China starts direct trading between the yuan and the New Zealand dollar on the inter-bank foreign exchange market.

March 17, 2014: The yuan's value is allowed to rise or fall by 2 percent from the central parity rate each trading day, from the previous limit of 1 percent.

April 9, 2013: China starts direct trading between the yuan and the Australian dollar on the inter-bank foreign exchange market.

June 1, 2012: China initiates direct trading between the yuan and the Japanese yen on the inter-bank foreign exchange market.

April 16, 2012: The yuan's value is allowed to rise or fall by 1 percent from the central parity rate each trading day, from the previous limit of 0.5 percent.

January 13, 2011: The PBC allows qualified domestic enterprises to invest in foreign countries directly using the yuan.

December 15, 2010: The yuan starts to trade in Russia, the first overseas market of the Chinese currency.

November 22, 2010: China initiates direct trading between the yuan and the Russian ruble on the inter-bank foreign exchange market.

August 19, 2010: China starts direct trading between the yuan and the Malaysian ringgit.

April 8, 2009: Cross-border trade is permitted to be settled in the Chinese currency on a trial basis in Shanghai and Guangdong Province.

May 21, 2007: The yuan's value is allowed to rise or fall by 0.5 percent from the central parity rate each trading day, from a previous limit of 0.3 percent.

July 21, 2005: China initiates reforms by depegging the yuan from the U.S. dollar. The PBC says it had shifted to a managed floating exchange rate based on market supply and demand with reference to a basket of weighted currencies. The yuan against the U.S. dollar appreciates by 2 percent to 8.11 on that day.

(Compiled by Beijing Review)

Copyedited by Calvin Palmer

Comments to zhouxiaoyan@bjreview.com |