| OPINION

Deposit Insurance: Fixing Eyes on Risk-Aversion

A long-anticipated insurance system for bank deposits will take effect on May 1. Superficially, it can insure savers' deposits; on a deeper level, it can caution savers to care more about avoiding risks instead of blindly pursuing high yields and awaken commercial banks to hold back from engaging in high-risk business and disordered competition.

Given the special role of commercial banks in the modern financial system and the possible destructive impact on savers' assets and the financial market caused by commercial banks' bankruptcy liquidation, the banking supervisory system should not only stimulate competition and business innovation but also reduce ethical risks to prevent banks from excessively raising interest rates or becoming obsessed with high-risk businesses. In this way, financial risks will not pile up and erupt.

Under competitive circumstances, commercial bankers are liable to wage price wars by raising deposit rates or cutting loan rates to attract more deposits, win more clients and achieve a higher performance. They may also engage in high-risk business to realize high profits.

When interest rates were rigidly controlled, commercial banks used to carry out price wars in disguised forms. As interest rate liberalization is underway these days, their "battles" have existed for a long time.

To some extent, price wars can significantly benefit depositors and borrowers, push commercial banks to enhance efficiency, and allow small banks to compete and gain a foothold by virtue of favorable interest rates.

However, if a price war gets out of control, it can squeeze the interest margins of commercial banks, and slacken their development momentum and vitality. As a result, all the commercial banks involved would suffer losses, trapped.

In extreme adversity, faltering or dying commercial banks are more motivated to attract deposits with high interest rates and invest funds in high-risk fields, because they have nothing to lose and a desperate struggle may help them ride out of the storms.

Such gambling behavior may press healthy commercial banks to participate in the cutthroat competition, because they would lose large numbers of clients if they stand by. From another perspective, if well-run commercial banks are forced into the game, their management efficiency would be undermined, profits would decline, and prospects would turn gloomy. No matter at home or abroad, there is no lack of such dangerous vicious competitions.

As a matter of fact, the above-mentioned ethical risks will break out only when depositors stop being vigilant. If depositors firmly believe their money will be unconditionally guaranteed by the government, they will be reluctant to know the real performance of commercial banks and identify the risks of newly released businesses. They will blindly embrace high interest rates and high yields, making it possible for these gambling-addicted commercial banks to absorb more deposits.

When China first began to practice the financial institution bankruptcy system in the 1990s, Hainan Development Bank and a number of financial institutions were shut down, showing its restriction on the ethical risks of commercial banks. Yet, since savers' deposits were intact, the ethical risks of depositors haven't been effectively constrained.

Against the liberalization of interest rates and the diversification of banking financial services, the introduction of a deposit insurance system will significantly constrain the ethical risks of both sides.

As far as savers are concerned, the policy will cover deposits and interest up to 500,000 yuan ($79,950). If excessively pursuing high interest rates and high yields, they will probably lose the part surpassing 500,000 yuan. Under such conditions, most savers will settle for safer money management schemes.

According to the newly released deposit insurance system, the insurance rates may differ based on factors such as lenders' operations and levels of risk. If banks adopt excessively aggressive strategies, their premium rates will be increased, which will raise an alarm and make savers reluctant to deposit money in these banks. In this way, the ethical risks of both commercial banks and depositors can be effectively constrained, and the risks in the financial system can be controlled.

This is an edited excerpt of an article by Mei Xinyu, an op-ed contributor to Beijing Review and a researcher with the Chinese Academy of International Trade and Economic Cooperation

NUMBERS

14.3 bln yuan

Sales revenue of L'Oreal, the world's largest cosmetics group, in China in 2014, an increase of 7.7 percent from 2013

20%

Revenue increase of Huawei Technologies Co. Ltd., China's leading communication technology company, in 2014

39.4%

Year-on-year decrease of the gross revenue of Macao's gaming industry in March, the 10th month in a row

11 bln yuan

Profit of China Pacific Insurance (Group) Co. Ltd., the country's third largest health insurance provider, in 2014, up 19.3 percent from 2013

745.24 bln yuan

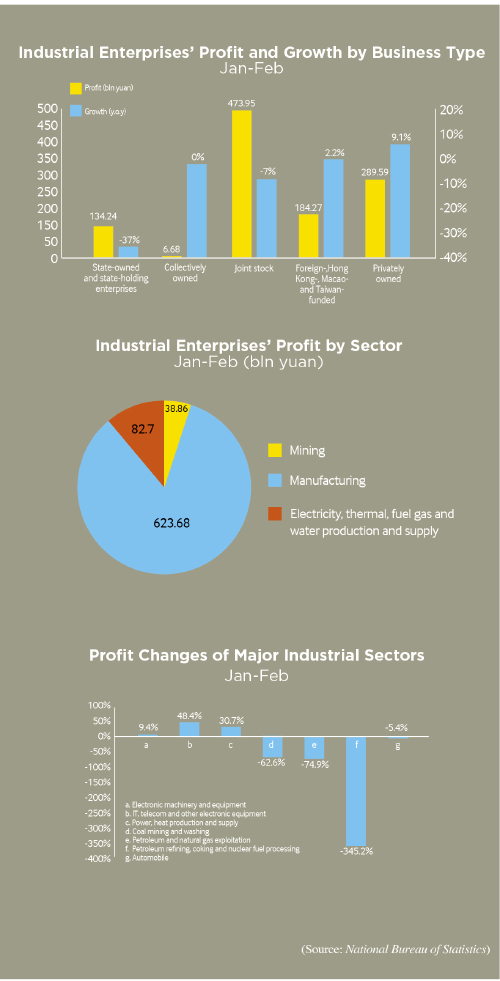

Profits from industrial enterprises above the designated size--principal business revenue of more than 20 million yuan ($3.2 million)--from January to February, down 4.2 percent year on year

5.5%

Proportion of Australia's trade with China in its GDP in 2014

34.21 mln tons

China's crude oil output in the first two months, up 1.2 percent from the previous year

76.7 bln yuan

China's service trade deficit in February, narrowing by a quarter from January

Copyedited by Kylee McIntyre

Comments to yushujun@bjreview.com |