|

| Business |

| Too Efficient to Fail | ||

| China plans to overhaul its state-owned enterprises | ||

|

||

|

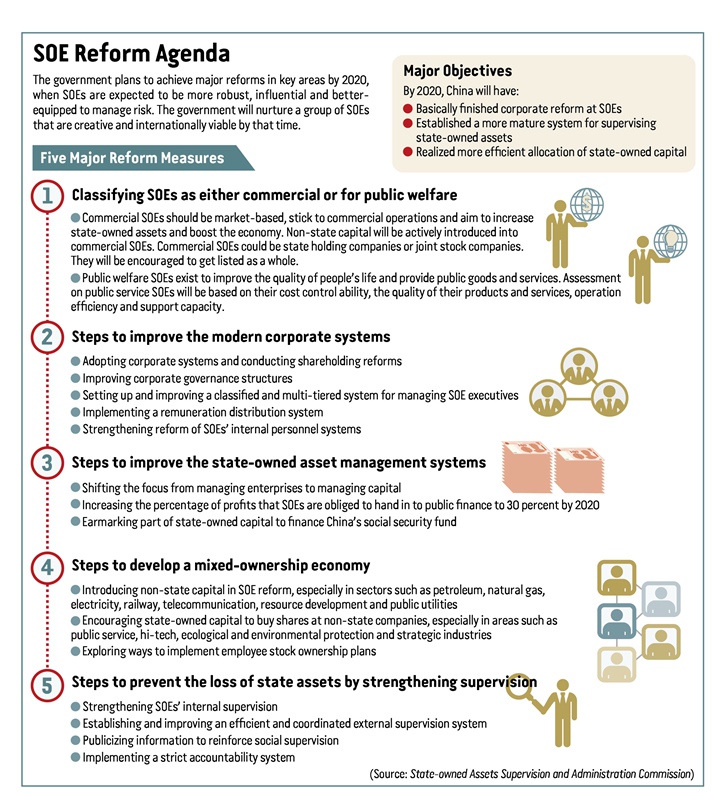

On September 13, China unveiled long-awaited details of how it would reform its state-owned enterprises (SOEs), the latest move to invigorate the country's torpid public sector by shaping a more pragmatic management system and nurturing more competitive public enterprises. According to the guidelines released by the Central Government, China will modernize SOEs, enhance state asset management, promote mixed ownership and prevent the erosion of state assets. In doing this, the government hopes to improve the competence of SOEs and turn them into fully independent market entities. "Decisive results in key areas of SOE reform are expected by 2020, when SOEs are expected to be more robust and influential and have greater ability to prevent and control risks," read the guidelines. "The government should have nurtured a large number of state-owned backbone enterprises that are innovative and can challenge international rivals by that time." Zhang Yi, Chairman of the State-Owned Assets Supervision and Administration Commission of the State Council (SASAC), the governing body of China's centrally administered SOEs, said that the goal of the reform is to enhance the overall efficiency of China's public sector. Li Jin, chief researcher with the China Enterprise Research Institute, said that the guidelines have one salient theme--to realize integration between state-owned assets and the market economy. "After the release of the document, mergers and acquisitions, and asset reorganizations among SOEs will accelerate," Li forecasted. The first top-level design for China's SOE reform in nearly two years, the guidelines touch upon several issues facing the reform, including classification of the massive number of SOEs, diversification of shareholders in SOEs, mixed-ownership reform, a more market-based salary system and stricter supervision of public enterprises. However, some analysts warned that since the document is instructive rather than mandatory, it will prove difficult to implement some of the policies as they will have to navigate the vested interests of involved parties.

Highlights SOEs have played a vital role in China's economic boom over the past four decades. There are currently 110 state-owned conglomerates administered by the SASAC, while many more SOEs are administered by local governments. A pillar of the economy, SOEs have enjoyed a dominant position in the market with easier access to cheap loans and more favorable policies, but a common complaint is a lack of efficiency--private firms have been more satisfactory in that respect--and the fact that they simply haven't delivered as much as expected since the economic slowdown took hold. In the first seven months of this year, the profits of SOEs declined by 2.3 percent year on year, according to data from the Ministry of Finance. The reform of underperforming SOEs has become one of China's most pressing needs amid a battle against downward pressure. "This reform will help to give an impetus to the economy and make growth more sustainable," said Xu Hongcai, Director of the Economic Research Department at the China Center for International Economic Exchanges, a Beijing-based think tank. One of the most significant innovations introduced by the guidelines will be a clear classification of SOEs into two categories, commercial and public welfare, to avoid a "one-size-fits-all" management approach. The former will be market-based and stick to commercial operations, aiming to consolidate state-owned assets and boost the economy; while the latter will provide public goods and services. Zhou Fangsheng, Deputy Director of the China Enterprise Reform and Development Society, said that classified regulation is the premise of modern corporate governance. "In the past, SOEs didn't have clear classification, and a less customized management approach created many problems," Zhou said. "For different types of companies, the managerial approach could be totally different. The two types of SOEs, for-profit ones and public welfare-related ones, will lay a foundation for future classified management," Zhou said. "The two parts will have differentiated reforms, development paths, supervision, responsibilities and systems of assessment," Zhou said. According to Zhou, the difficult part is distinguishing between China's tens of thousands of SOEs. "In many SOEs, especially centrally administered behemoths, there exist both commercial and public welfare-related assets. Some assets are commercial entities masquerading under the guise of public service providers. Specific classification will take some time and involve interests of several different parties," Zhou said. "After finishing the classification, the two types of SOEs should be forbidden from investing in each other's businesses," Zhou suggested. The latest guidelines call for a greater focus on SOEs' capital returns and greater tolerance with so-called mixed ownership, or the participation of private investment in existing public companies. State firms will be allowed to bring in various types of investors to help diversify share structure, and more state firms will be encouraged to restructure to pave the way for stock listings. Private investors will be encouraged to buy stakes in state firms, to buy SOE-issued convertible bonds or to swap shares with their public counterparts. According to the guidelines, SOEs will also be allowed to experiment with selling shares to their employees. In addition, the document states that the government will not force mixed ownership, nor will it set a timetable, giving each firm the go-ahead only when conditions are ripe. Zhou said that mixed ownership and employee shareholding programs will result in a diversification of shareholders and help provide a rationale underlying the corporate-level decision-making process. "In the future, China will be more cautious toward the reform. Mixed-ownership reform is not equal to privatization but should be carried out only when it can make SOEs stronger and better," warned Zhu Zhenxin, a researcher at Minsheng Securities Co. Ltd. "From here on in, private capital will be introduced on the basis of preventing the loss of state assets and promoting the augmentation of state assets." A change of managerial thinking toward state assets is another theme of the guidelines. According to the document, the state-owned asset management system will shift from managing enterprises to managing capital. Wang Jun, another researcher at the China Center for International Economic Exchanges, said that indicates a fundamental change in the role of the SASAC. "The SASAC used to micromanage SOEs--managing their assets, personnel and even daily operations. In the future, it will be reoriented toward dictating rules that preclude, for instance, improper intervention from the government, which will greatly boost the vitality and efficiency of business operations," Wang said. The guidelines also require SOEs to strengthen the system that prevents boards of directors being unduly influenced by top executives, and the introduction of more flexible and market-based wage and human resource systems at state firms through the linking of pay with company performance. It is also noted that supervision over state-owned assets should be tightened during the process of SOE reform to ensure asset security. Tough task Xu Baoli, a researcher at the SASAC's Research Center, said that SOE reform will engender many opportunities and face many challenges, as central authorities will have to persuade entrenched interests within local governments to relinquish some control over state firms. The guidelines are directives rather than steadfast rules, he said. Li, chief researcher with the China Enterprise Research Institute, said that SOE reform is all about redistributing interests; therefore, policy implementation may prove difficult. "For instance, the guidelines say no shareholding limit should be set for private capital for SOEs if those companies are in a fully competitive sector. Private firms would rush in to grab a piece of the action, availing themselves of profits on a scale previously enjoyed only by SOEs. Therefore, public companies will be quite reluctant to carry out that policy," Li said. "Now that the top-level design has been released, local governments should focus on how exactly to implement it," Li said. "SOE reform entails a different task for local governments than it does for the Central Government. SOE reform carried out by local governments have to be tallied with other thorny issues they face--dealing with a hefty amount of debt, clearing their financing platforms and reforming their fiscal and taxation policies. Therefore, for them, SOE reform is even more pressing. Merger and acquisition, and asset reorganization are important means of accomplishing reform goals." Zhou, Deputy Director of the China Enterprise Reform and Development Society, said that it's a pity that the guidelines do not address the much-mooted reform of dividend rights at SOEs. According to Zhou, reform of China's Lenovo Group, the world's largest PC maker and one of the top smartphone makers, started from giving employees the right to enjoy dividends. "Without reform of dividend rights, Lenovo wouldn't have become as strong as it is. If a SOE is in a fully competitive market, its employees should be granted the right to dividends. Having access to the value they create and letting them play a part in steering the company will greatly motivate them," Zhou suggested. Like China, many other countries have undertaken reform of their public enterprises. However, Cao Heping, an economics professor at Peking University, said that China's SOE reform cannot merely parrot the approach of other nations. "China's situation is much more complicated than that of any other country in the world, therefore China has no model to use as a suitable template. For instance, some people said that we should derive inspiration from Singapore's Temasek model. That would be totally unfeasible," he said. "Singapore is only half the size of the Binhai New Area of north China's port city of Tianjin and there, one centralized state-owned asset management agency can effectively govern its state assets. While in China, the situation is totally different. Only by establishing a sound primary market and secondary market can effective capital exchange be realized to invigorate state assets." Copyedited by Kylee McIntyre Comments to zhouxiaoyan@bjreview.com |

|

||||||||||||||||||||||||||||

|