|

| Business |

| Exploring Opportunities amidst Challenges | |

| Chinese economy levels off at 6.7 percent in 2016 with optimized structure, despite uncertainties ahead | |

|

|

|

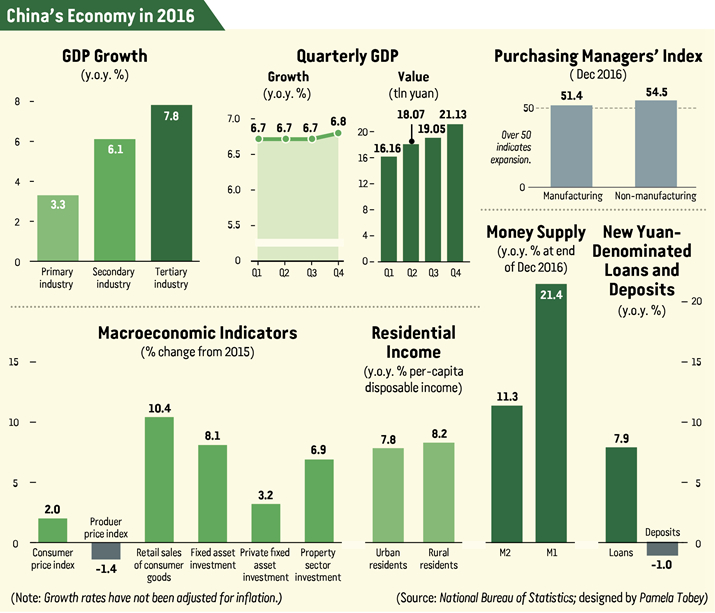

A technician at work at a laser remanufacturing plant in Qianan, Hebei Province, on November 12, 2016 (XINHUA) China's economy grew by 6.8 percent in the fourth quarter of 2016, following a 6.7-percent expansion in the previous three quarters. Meanwhile, the annual growth rate stood at 6.7 percent, accompanied by structural improvement, transformation of development models and the emergence of new growth engines. "As the world's second largest economy, China's economic aggregate has reached $11 trillion, which means there is a significant increase in economic aggregate for every 1-percent increase in the GDP," said Ning Jizhe, Director of the National Bureau of Statistics (NBS), at a press conference held on January 20. As calculated through a constant determined by the 2010 dollar, China contributed 33.2 percent to global growth in 2016, remaining the world's top driver of growth, according to a statement released by the NBS on January 13. China also regained its position as the world's fastest-growing major economy in 2016, as India, another major developing economy, registered a growth rate of 6.6 percent, according to the International Monetary Fund. Furthermore, the country's economic structure is continuously optimizing. In 2016, the service sector continued expanding faster than other sectors and consumption contributed roughly two thirds to total growth. Hi-tech industries also saw accelerated development, and industrial energy consumption per unit of GDP decreased 5 percent, according to the NBS. China's overall economic growth continued to slow down in 2016 compared to previous years as the country has entered a "new normal" economic state. Nonetheless, as ongoing supply-side reform keeps generating positive results, and as infrastructure investment, housing, and automobile demand picks up, the macroeconomy has shown signs of stabilizing, said Yan Yan, Deputy Director of the School of Economics of Renmin University of China, in an interview with National Business Daily. Yao Jingyuan, a research fellow from the Counselors' Office of the State Council, told that it wasn't easy to return the producer price index (PPI) and industrial profits to positive levels. Last September, the PPI—a measure of costs for goods at the factory gate—rose 0.1 percent, reversing a negative growth trend that had run for 54 consecutive months. Moreover, the profits of enterprises above a designated size—with principal business revenue of more than 20 million yuan ($2.91 million) a year—increased over 9 percent in 2016, in stark contrast to the negative 2.3 percent registered in 2015. Yao explained that the turnaround in 2016 occurred due to real results from policies and measures designed to stabilize growth, surging domestic demand, and progress in the decapacity campaign. Last year, the decapacity goals for the iron, steel and coal industries were overfulfilled. Due to reduced supply, rising demand and an improved external environment, prices in those sectors rose, leading to enterprise profits bottoming out, Yao said.

The No.2 blast furnace of Baogang Group is dismantled in Baotou, Inner Mongolia Autonomous Region, on August 31, 2016, as part of the efforts to cut iron and steel overcapacity (XINHUA) Capacity reduction In 2016, China had managed to cut 45 million tons of iron and steel production capacity and 250 million tons of coal production capacity, with its annual raw coal output declining 9.4 percent, according to the NBS. While satisfactory results have been achieved in cutting overcapacity, some problems still need proper solutions, Yao said. According to Yao, the completion of the decapacity goal depended mainly on administrative measures, which are efficient but not entirely reliable. For instance, as the price for iron, steel and coal rebounded in the second half of last year, some shutdown production facilities returned to operation without sufficient safety preparations. This led to some major safety accidents. Cutting overcapacity should be pursued through more market-based and law-based measures, and be closely integrated with restructuring efforts, said Yao. During the decapacity process, a market-oriented mechanism fostering the survival of the fittest and fair competition should be established. Otherwise, when prices rebound, some low-end capacity companies may restore their production, which will go against the restructuring process, Xu Hongcai, Deputy Chief Economist at the China Center for International Economic Exchanges, told Beijing Review. Besides that, workers who are laid off due to overcapacity reduction will put pressure on the nation's employment. According to statistics from the Ministry of Human Resources and Social Securities, decapacity measures will affect 500,000 and 1.3 million workers in the iron and steel and coal industry, respectively. Employment in the cement, glass, electrolytic aluminum and shipping sectors are also likely to be affected. Real estate The property market was a strong contributor to the overall economy in 2016. However, since an array of regulatory policies were launched last September and October to suppress the skyrocketing housing market, real estate sales and investment have shown signs of stabilizing. According to statistics from the NBS, 12 of China's 15 major cities saw a month-to-month decline in housing sale prices while two cities held the line, and only one city experienced a month-to-month increase. "So far, the real estate market fever has been assuaged," said Ning. In regulating the housing market, the government should control speculation and the precipitous rise of housing prices, and meanwhile, give consideration to the polarization between large cities and third- and fourth-tier cities, said Ning. In major cities, housing prices kept shooting up, while in third- and fourth-tier cities, inventories were still high. Therefore, different measures and policies should be launched to tackle different problems in different regions, said Ning, who believes China's real estate market will maintain healthy development in 2017. Under the influence of housing purchase restrictions, inventory pressures and changing supply-demand relationships, the real estate market will enter a stage of restructuring and adjustment in 2017, which will add downward pressures on the economy, said Yan. Li Chao, chief researcher on the macroeconomy with Huatai Securities, told that regulatory policies will gradually affect housing sales, which will further bring down investment in real estate sector.

Lurking risks Despite the stable and sound development witnessed in 2016, internal and external economic circumstances are still complicated, and the foundation for stable and sound growth in the future is still weak, according to a statement by the NBS. Although China's economy had shown a tendency of bottoming out, it needs time to see whether the trend can be sustained. This is because to a large extent, the economic achievement registered in 2016 was primarily due to the surging housing market and the recovering export was basically driven by stronger overseas demand. The economy still lacks new growth engines, said Xu. Aside from that, Yan suggested that attention should be paid to two new uncertainties that emerged in 2016—soaring prices of raw materials and rising enterprise financing costs. In addition, in 2016, private fixed-asset investment increased only 3.2 percent, falling short of one third of the pace in 2015. Private fixed asset investment is gloomy, and private investors' confidence still needs to be restored, said Xu, who suggested that the government should put in place a market mechanism fostering fair competition when pushing forward mixed-ownership reform among state-owned enterprises (SOEs). A similar mechanism should be employed to break the monopoly in the petroleum, natural gas and telecommunications industries, spark the innovative impetus and vitality of SOEs and expand room for private investment. In addition, though the overheated growth of the property market in first-tier cities has been kept in check, a long-term mechanism should be established to ensure the healthy development of the market, said Xu. At the same time, efforts to carry out the five major tasks of the supply-side structural reform, namely, cutting overcapacity and excess inventory, deleveraging, reducing costs, and shoring up weak growth areas were unsatisfactory at times. Some tough issues were left behind, said Xu, noting that real progress should be made in 2017 to solidify the foundation for healthy economic development in the long run. In 2016, China's foreign exchange reserve went down by $319.8 billion, which is less than the decrease observed in 2015. But considering the United States Federal Reserve's plans to raise interest rates and the rapid flow of outward investment from Chinese enterprises, there are still risks in capital outflow and yuan depreciation, said Zhang Ming, a research fellow on international investment with the Institute of World Economics and Politics, Chinese Academy of Social Sciences. The focus of macroeconomic regulation in 2017 has shifted from stabilizing growth to risk prevention, said Zhang. Copyedited by Bryan Michael Galvan Comments to dengyaqing@bjreview.com |

|

||||||||||||||||||||||||||||||

|