|

| Business |

| A Global Network | |

| Belt and Road Initiative is attracting more countries for a larger community of shared future for mankind | |

|

|

|

In an exclusive interview with Beijing Review, Henry Tillman, Chairman and CEO of Grisons Peak, a London-based merchant bank,shared his views on a range of topics from the development opportunities the Belt and Road Initiative has produced to the misunderstandings toward it. Edited excerpts of the interview follow:

Beijing Review: How do you think China has shared development opportunities with countries along the Belt and Road routes under the Belt and Road Initiative?

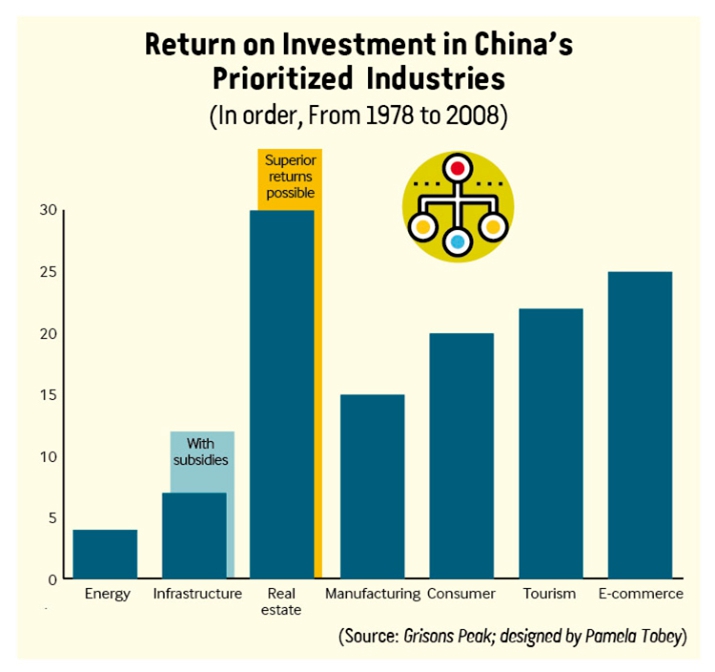

The attached graph shows that in order to develop more advanced and profitable industries such as manufacturing, tourism and e-commerce, a country needs to have adequate energy and infrastructure, which includes technology, railways, highways, ports and logistics. The development of these gives rise to significant real estate investment opportunities, sometimes producing above average returns. A number of countries involved in the Initiative have already made considerable gains in adding new energy and infrastructure including Cambodia, Laos, Sudan, Ethiopia, Kenya and Pakistan, to name just a few. Pakistan has produced 7,000 megawatts of new energy in just over three years with another 10,000 megawatts expected to become operational within the next three. All its main motorways are expected to be operational by the end of next year. With adequate energy, special economic zones (SEZs) are now being designed to grow manufacturing in Pakistan, which has also been able to attract substantial corporate capital since 2016. The five countries of the Greater Mekong Subregion (Cambodia, Laos, Myanmar, Thailand and Viet Nam) have all signed Belt and Road agreements. The China-Laos railway, China-Thailand railway and China-Myanmar land-water transportation are in development. These railways, linking Kunming with the Mekong Delta and into Malaysia and Singapore, should be operational within the next five to seven years. A good European example of a win-win project is Piraeus Port in Greece, one of the largest ports in the Mediterranean and in Europe. Before China Ocean Shipping (Group) Company (COSCO) became involved, container flow was only 1.5 million TEUs per year at the port. In 2017, container flow increased to 3.7 million TEUs. According to a joint statement by the foreign ministers of China and Greece, Piraeus Port's global ranking has climbed to 36 from 93 in 2010. Fifty-five shipping lines with the port as their hub have a far-reaching impact on the Mediterranean and connect various continents in the world. There are 16 to 18 freight trains departing from Piraeus Port for Central and Eastern European countries every week. Piraeus Port's direct economic contribution to Greece has exceeded 600 million euros ($700 million), with more than 10,000 job opportunities being created. Some developed countries, such as the UK, as well as large multinational corporations, have expressed interest in participating in the Belt and Road Initiative in the form of third-party market cooperation. How have they worked with China under the initiative in recent years? While the UK and many other European countries have not yet signed official Belt and Road partnership agreements, several of these countries are actively participating in the initiative. During Q1 2018, China and the UK committed to increasing cooperation in fintech (the UK led the world in fintech investments in H1 2018). Chinese investors also pledged over 1 billion euros ($1.16 billion) in funding to two British venture capital firms. In December 2017, Standard Chartered agreed to lend at least $20 billion in financing to Belt and Road projects by 2020 and in February 2018, the China Development Bank agreed to make $1.6 billion available in the next five years to Standard Chartered to facilitate Belt and Road projects. HSBC has also been active in green finance, while the London-Shanghai stock connect program is expected to be launched in late 2018. The UK also possesses a lengthy track record with many Central Asian countries, including Pakistan, Bangladesh and Kazakhstan, in government, investment and business, as well as with many African countries, which could assist future Chinese investment in such countries. China is in discussions with Luxembourg to build a Silk Road in the air, while the Netherlands and China have been discussing how the former could play a role as a key EU logistics hub. Recently, our firm has been analyzing 28 investments from China in Germany during the period 2010-14—approximately 4 billion euros ($4.65 billion) aggregate value—as well as 17 investments from German companies into China in 2000-14. There have been numerous successes in each direction. Chinese investment in KION Group and Linde has helped transform these companies, as well as at Preh, Putzmeister and SCHWING. However, these pale in comparison to the 60 billion euros ($69.74 billion) plus that Germany has invested in China to date, led by large joint ventures, some dating back to the early 1980s, involving Volkswagen, BMW, Daimler, Bosch, Allianz and BASF. In June 2018, Siemens, which has operated in China for over a century, entered into a formal agreement involving a number of major Chinese state-owned enterprises for Belt and Road projects in Indonesia, the Philippines, Nigeria, Mozambique and countries in Latin America. In 2017, Deutsche Bank signed a memorandum of understanding (MoU) with the China Development Bank to jointly fund $3 billion of Belt and Road projects before the end of 2022. In July 2018 Commerzbank signed an agreement with ICBC to lend $5 billion to Belt and Road projects in partnership with ICBC. As a multilateral development bank which plans to invest in sustainable infrastructure and other productive sectors in Asia and beyond, what has the Asian Infrastructure Investment Bank (AIIB) achieved since its inception? How has it interacted with other financial institutions such as the World Bank and the IMF? The AIIB was launched in January 2016 with 57 members, and as of June 30, 2018, had 87 members. The AIIB has been very active in building partnerships to syndicate credit on deals it underwrites to partner banks. This includes a co-financing agreement with the World Bank signed in April 2016 as well as MoUs signed with the European Bank for Reconstruction and Development the same month, the Asian Development Bank and the European Investment Bank in May 2016, the International Bank for Reconstruction and Development in April 2017 and the Islamic Development Bank in June 2018. Two recent deals are good indicators of future trends. One is a $140 million commitment on a $502 million credit facility for road improvements in India (the World Bank underwrote $210 million), while the other is a $100 million investment in a $600 million Indian fund of funds focused on infrastructure. It is worth noting that this loan and investment represent the sixth and seventh loans to India since Q1 2017—the seven loans represent 25 percent of AIIB's total loans since its inception. Much of China's Belt and Road investment is in infrastructure, which will have a long-term effect on economic growth, livelihoods, jobs and tax revenues in those countries. However, there are concerns about the increasing debt burden of those countries, with suggestions that China is setting a "debt trap" for these governments. What is your opinion? China's funding structures are well crafted and are packaged to include numerous components such as senior debt, often with several year grace periods aligned with revenue production (as in Kyrgyzstan), grants, mezzanine finance and equity from various Chinese sources, including regional Chinese led equity funds and the Silk Road Fund, as well as Chinese corporates and construction companies. While Chinese policy banks used to be the lowest rate senior loan provider (2-3 percent interest rates) with long maturities (20-plus years), Japanese lenders have recently issued loans at much lower rates (as low as 0.01 percent) up to 40 years. Meanwhile Chinese policy banks, commercial banks and the AIIB are increasingly underwriting loans they can syndicate to global banks at market rates. For the past few months, many publications have discussed a "debt trap." The ratios from some of African countries most cited demonstrate that in fact they are well below some European countries in debt/GDP ratio and actually declining: Ethiopia, 34.9 percent in 2016, declining to 33.5 percent in 2017; Zambia, 68.4 percent in 2015, declining to 55.6 percent in 2017, and Angola, 75.8 percent in 2015, declining to 65.1 percent in 2017. While the Democratic Republic of Congo showed 117.8 percent in 2017, it was still well below Italy's debt/GDP ratio—132 percent—and Greece's 180 percent. In addition to its long-term strategic partnerships, China takes a portfolio investment approach for each Belt and Road country. It is true that there are some projects in Sri Lanka which have underperformed to date. However, these projects need to be analyzed as part of the whole package. The country's Colombo Port was named Asian port of the year in 2017 for ports below 4 million TEUs. The China Merchants joint venture showed 21.2-percent growth in 2016 and 18.5 percent in 2017 in its accounts from Colombo Port. What do you foresee for the next five years? In the past year, two new routes—the Polar Silk Road (PSR) and the Pacific Maritime Silk Road (PMSR)—have been discussed. The PSR is designed to ship liquefied natural gas produced in north Russia both east to China as well as west to Europe via the North Sea. During the past month, five Chinese ships, led by Russian Yamal icebreakers, made this journey in less than 50 percent of the time it would have taken via the Suez Canal. Yamal 1 is already operational while Yamal 2 is expected to be so in 2023. The PMSR appears to be a variation of a 16th century Asian trade route which passed through the Philippines and Mexico before continuing to Spain. The 21st-century version is likely to enter Peru, and will also likely end in Europe. Options include Portugal, which is a key hub for the Latin American and Caribbean region and West Africa, as well as Spain, with its links to Morocco and Algeria. With investment increasing over the past year, it is also reasonable to expect more collaboration involving Khalifa Port and the Dubai SEZ in the United Arab Emirates, as well as Turkey, with Istanbul as a future logistics hub for the Silk Road Economic Belt. Last but not least, it is likely that India will play an increasing role in the Belt and Road Initiative over the next five years, which could lead to a new Economic Corridor or Silk Road, also involving Nepal.

Copyedited by Laurence Coulton Comments to zhouxiaoyan@bjreview.com |

|

||||||||||||||||||||||||||||||

|

Henry Tillman: The first five years of the Belt and Road Initiative need to be viewed as the initial steps of a long-term project, centered around economic and trade development and augmented via education along the Belt and Road routes and in individual countries and regions.

Henry Tillman: The first five years of the Belt and Road Initiative need to be viewed as the initial steps of a long-term project, centered around economic and trade development and augmented via education along the Belt and Road routes and in individual countries and regions.