|

| Business |

| App-and-Coming | |

| Mobile applications become banks' new golden goose | |

|

|

A woman uses a smart counter to handle business on her own in a bank in Wuzhen, east China's Zhejiang Province, on November 9, 2018 (XINHUA)

Checkbooks can be called the dinosaurs of banking. Once essential for transactions, especially those involving large sums of money, they became virtually extinct with the arrival of ATM cards. Now, as technology continues to evolve, it could be time to say goodbye to the handy little bankcards as well. "These days, most transactions can be done using mobile apps," Zhao Jingyi, a Beijing resident who has an account with China Merchants Bank (CMB), said. Zhao hardly needs to take her bankcard with her when she goes to a CMB branch these days. "Customers can make an appointment in advance through the CMB's app so that they don't have to wait on-site," she said. "Or they can use the app to get their number in the queue of customers and instead of having to wait at the bank in person, can take care of other work before their turn comes, like shopping or even eating out. They receive a message from the bank when their turn comes and can then make their way to the bank counter." Many banks have installed equipment with face recognition technology, like China Construction Bank (CCB), and customers can withdraw money from the ATMs without using a bankcard and do other transactions at a designated smart counter. But some banks are still proceeding cautiously with this new technology. At branches of Bank of China (BOC), for instance, customers need to produce an identity card, though not the bankcard. "The bankcard is a static product whereas mobile apps stand for a whole ecosystem," Liu Jianjun, Vice President of the CMB, said. Liu said apps are facilitating interactions between banks and their customers. They can give users easy access to all the banking services on offer, ranging from transferring money to paying bills and buying wealth management products. It is foreseeable that in the future there will be fewer scenarios for people to use bankcards, and a card-free age is about to come. It will effectively slash customers' time cost and also banks' and merchants' operation costs related to point-of-sale systems. To make that happen, more banks need to use Internet-based tools, innovative ideas and cutting-edge technologies.

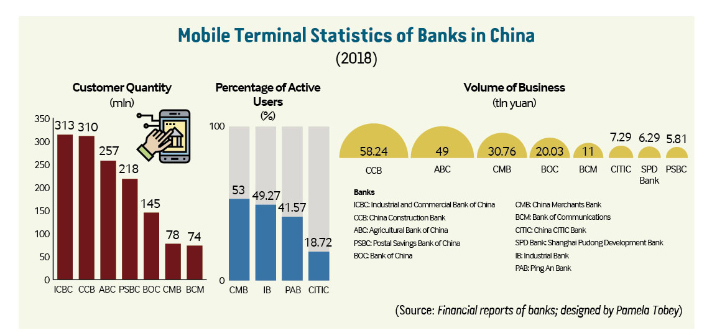

Retailing 3.0 Mobile apps replacing bankcards as the main method of transactions marks the banking industry's advent into the age of retailing 3.0. Tian Huiyu, President of the CMB, summed up the evolution. "For the CMB, if retailing 1.0 signifies a transformation from the bankbook to the all-in-one card, that is, the debit card, then retailing 2.0 marks a shift of its business focus from attracting deposits to wealth management services, and the ongoing retailing 3.0 is seeing mobile apps replace bankcards," he said. Retailing has become the most critical part of the banking industry's transformation. It constitutes more than half of the profit of some banks and the proportion is getting larger, indicating that this business has become the new hot cake as well as the battlefield for banks' future growth. Statistics from Ping An Bank show that in 2018, retailing accounted for 53 percent of its total revenue and 69 percent of its net margin. The CCB's profit from the retail business in 2017 was nearly seven times that in 2008. To be more precise, the retailing 3.0 battlefield is becoming concentrated on the competition among the mobile apps of different banks. According to a report issued by the China Financial Certification Authority, a software publisher under China's central bank, a survey in 2018 found 57 percent of the respondents were mobile banking app users while 53 percent preferred online transactions. It was the first time mobile banking had exceeded online banking on the user scale, becoming the most important platform for banks to approach their customers. Banks have stepped up efforts to build up their mobile banking ecology, focusing on shifting retail businesses to digital platforms and strengthening the service capacity for robust growth. In 2018, the number of mobile banking customers of the Industrial and Commercial Bank of China and the CCB exceeded 300 million, with the CCB's mobile business volume hitting 58.24 trillion yuan ($8.46 trillion). Of all the Chinese banks that disclosed their percentage of active mobile app users, the CMB topped with a rate of 53 percent. According to iResearch, a market research and consulting company, a study of China's Internet traffic in the first quarter of this year showed that financial service apps, including mobile banking, ranked among the top 10 categories of apps in terms of utility time. While maintaining high usage frequency, they also registered a high growth rate. It was found that the monthly and daily utility time of financial service apps increased by 40.2 percent and 18.6 percent year on year, respectively, in the first quarter. Opportunities in technology However, bank apps lack the advantages third-party payment apps like Alibaba's Alipay and Tencent's WeChat Pay have, whose functions such as money transferring, bill payment and wealth management services are already mature. Therefore, they need to integrate existing resources and strike out in a new direction. Some banks are developing apps exclusively for different segments. For example, the BOC has launched an app for senior people to manage their assets. Many banks have also realized that the habit of investing small amounts and buying simple wealth management products on mobile phones will ultimately direct more and more people toward buying large-amount products on their apps as long as there is a more diversified portfolio of products, and a more flexible choice on the investment cycle, the purchase amount and redemption policies. The Industrial Bank has therefore developed a platform where more than 400 other banks can post and run their wealth management services. The CMB introduced its card-free plan in 2014, and in 2018, the wealth management products sold on its app reached 6.26 trillion yuan ($910 billion), up 41.3 percent year on year, accounting for 60 percent of its total wealth management sales. "In 2019, the CMB will focus on product upgrading and promote mobile services to advance card-free development," a CMB spokesperson said. Although challenges remain in competing with Internet companies, banks can still find opportunities in technology. "Technology is the only method to fundamentally change and overturn banks' business model," Tian said in the CMB's 2017 annual report. He also pointed out that financial technology (fintech) is the most efficient way for banks to transform and establish a better business model. Currently, a lot of customers complain that bank apps' speed of operation is very low due to the large volume of data. However, the development of 5G is expected to help bank customers to access their mobile terminals faster and with wider coverage. On June 5, the BOC launched a new version of its mobile bank app, integrating technologies including cloud computing, big data and artificial intelligence. The result is services such as intelligent risk control and smart algorithms, making it both an assistant and a financial consultant for customers. Zheng Guoyu, Vice President of the BOC, said technology is empowering banks by changing their traditional way of operation and serving customers. "Mobile banking is crucial for the BOC's strategic transformation," he said, "The tide of fintech is approaching us and we should seize the momentum, keep pace with the changes and embrace technological reform." Copyedited by Sudeshna Sarkar Comments to dengyaqing@bjreview.com |

|

||||||||||||||||||||||||||||||

|