|

| Business |

| Return of foreign-listed Chinese firms sees China Concepts Stocks trending | |

|

|

Chinese Internet technology company NetEase makes its secondary listing in Hong Kong on June 11 (XINHUA)

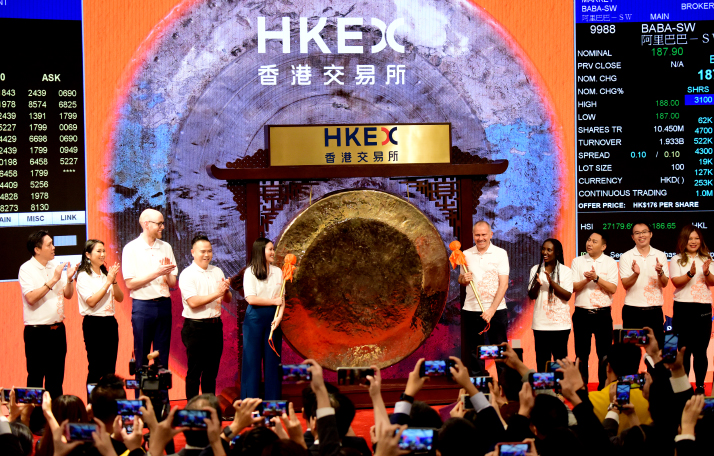

In 2000, when a 3-year-old Chinese Internet technology company called NetEase made its debut on the Nasdaq, the results were far from spectacular. Its stock price declined continuously and it was delisted for four months due to financial problems. Ding Lei, its founder, said he wanted to sell the company. Twenty years later, it is another story. NetEase today is one of the world's largest Internet companies and on June 11, Ding rang the bell for the company's second listing on Hong Kong Exchanges and Clearing Limited (HKEX). Due to the novel coronavirus, it was a cloud listing done from the office of NetEase in Hangzhou, Zhejiang Province in east China. A total of 171 million new shares were issued at the price of HK$123 ($15.87) per share, one of the largest-scale stock offerings on HKEX this year. On the first day of trading, the price rose by over 8 percent. The second listing put NetEase in the group of Chinese companies that first listed outside the Chinese mainland to facilitate foreign investment and are known as China Concept Stocks (CCSs). And now the CCSs are returning home. NetEase became the second CCS after tech giant Alibaba to have a second listing on HKEX. Then on June 18, another e-commerce giant, JD.com, followed suit, indicating CCSs returning is now a trend. "More CCSs will have their second listings on HKEX within the year and they are expected to be listed on the A-share market as well in the future," Lin Guoen, a partner at Deloitte China, said at a press conference on June 16 following the release of a review of the first half-year IPO markets of the mainland and Hong Kong.

Ten cooperative partners are invited to ring the ceremonial bell to start trading during e-commerce giant Alibaba Group's debut on the main board of Hong Kong Stock Exchange on November 26, 2019 (XINHUA) Anticipated return Dong Dengxin, Director of the Finance and Securities Institute, Wuhan University of Science and Technology, attributes the trend to two reasons. Early in 2018, HKEX and the China Securities Regulatory Commission (CSRC) started reforms, paving the way for the trend, he told Beijing Review. Also, U.S. restrictions on Chinese hi-tech companies like Huawei have affected their operation in the U.S. market with the specter of delisting hanging over them. This means they will explore other markets now. "In the past, many Chinese companies chose to list on the U.S. stock markets because HKEX had stricter requirements on issues such as corporate governance and weighted voting right (WVR) structures," HKEX Chief Executive Charles Li said on June 6. The approval-based IPO system in the A-share market, in which the CSRC vetted every application, also raised the threshold for the companies looking to list there. However, in 2018, HKEX proposed new IPO rules to allow companies with WVR structures. It also established a new concessionary secondary listing route for companies based in the mainland, Hong Kong, Macao and Taiwan, and abroad, wishing for a second listing in Hong Kong. In addition, it allowed biotech companies that did not meet the financial eligibility criteria of the main board, the most important board in the A-share market designed for the listing of large-scale companies. "The new rules have basically reformed the listing regime and will make listing more flexible," Li said. The CSRC has also been rolling out measures since 2018 to lower the A-share market's listing threshold. Currently, innovative red-chip companies, or companies registered overseas but operating on the mainland, enjoy a lower threshold to list or issue China depositary receipts. In addition, the Science and Technology Innovation Board (STAR Market) launched in 2019 has opened specific channels for red-chip companies and companies with WVR structures to trade on it. External events have also become a catalyst for Chinese companies' return. On May 20, the U.S. Senate approved the Holding Foreign Companies Accountable Act to bar foreign companies operating on U.S. stock exchanges if they flout Securities and Exchange Commission oversight. It requires Chinese companies to establish that they are not owned or controlled by a foreign government and to submit to an audit that can be reviewed by the Public Company Accounting Oversight Board (PCAOB), the nonprofit body that oversees the audits of all U.S. companies seeking to raise money in public markets. In other words, if Chinese companies refuse to be reviewed by the PCAOB, they will not be allowed to apply for IPO or can be delisted. Besides, there are other obstacles for CCSs in overseas markets. Lack of regulation has made them targets of overseas short-selling speculators, which affects investors' confidence for long-term investment. Also, since they have different business models, it is often difficult to explain their advantages to overseas investors. So except for a few high-caliber companies, most remain undervalued. All these factors have led to a return momentum. Impact of Chinese markets The trend will also impact the development of the Hong Kong and A-share stock markets. "The return will benefit the Hong Kong stock market in the long run as it will introduce new funds and capitals to the market," Chen Li, chief economist of Soochow Securities, said. Currently, the market value of financial companies on the board of HKEX accounts for over 30 percent of the total. With more companies returning, the mix of companies listed on the board will become increasingly diversified. Xia Chun, chief economist with Noah Holdings, a financial service provider, told Economic Daily that investors in the A-share markets also hope to buy high-quality assets through stock connect schemes such as the Shanghai-Hong Kong Stock Connect. Since most CCSs are high-quality information technology companies, their return could make southwards trading more frequent and improve the overall valuation of Hong Kong stocks. Lin said if new listing rules can be issued in the second half of the year to shorten the time taken for new share issuance, Hong Kong's competitiveness as an ideal listing place for Chinese companies would increase. As for the impact on the A-share market, Li Qilin, chief economist of Yuekai Securities, said in the short run, the massive return of companies to HKEX will divert some capital from the A-share market, especially from technology stocks whose value were overestimated, but in the long run, the impact will be positive. The listing of high-quality CCSs on HKEX will drive overseas investors to pay attention to the A-share market, which will increase the valuation and liveliness of the technology and new economy sectors in the market. Moreover, as the STAR Market implements a registration-based system for listing and the infrastructure of the capital market improves, the stocks could also list on the A-share market. (Print Edition Title: Time to Take Stock) Copyedited by Sudeshna Sarkar Comments to zhangshsh@bjreview.com |

|

||||||||||||||||||||||||||||||

|