|

| Business |

| Against the Current | |

| The internationalization of the renminbi progresses amid exchange rate fluctuations | |

|

|

|

Pedestrians walk past a Bank of Communications branch in Hong Kong on February 24, 2017 (XINHUA)

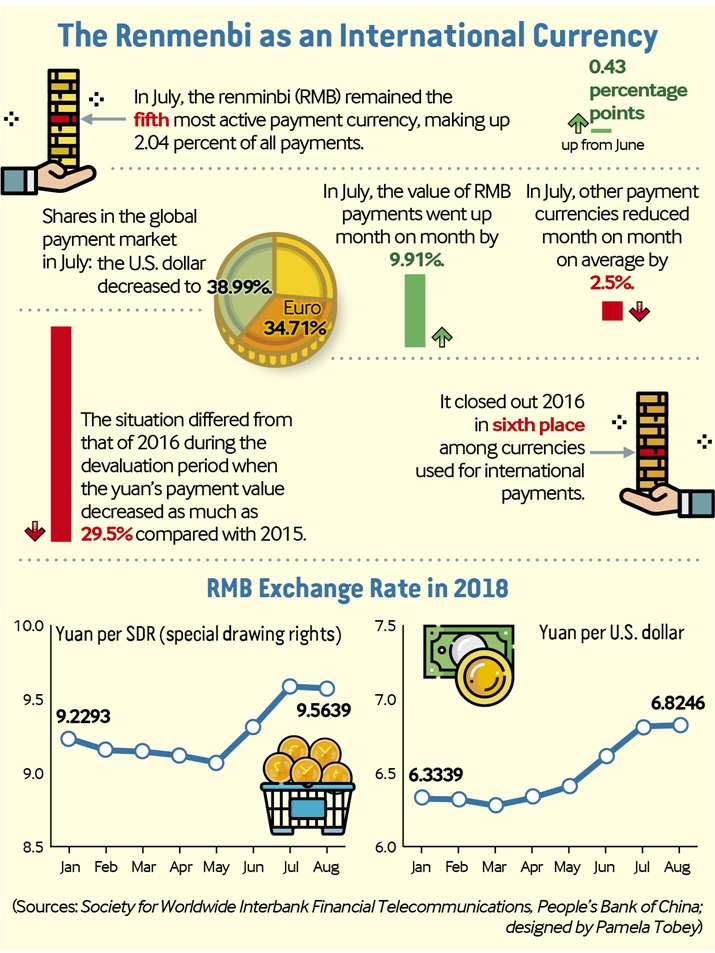

When the United States announced that it will impose an additional 10-percent tariff on $200 billion worth of Chinese products effective on September 24, the news further stirred the Chinese exchange rate market as 2018 has witnessed the ebb and flow of the renminbi exchange rate. The yuan has depreciated by nearly 7 percent since mid-June, when the United States first made the new tariff threat, a signal of escalating Sino-U.S. trade tensions. However, according to data released by the Society for Worldwide Interbank Financial Telecommunication (SWIFT) in August, the renminbi remained the fifth most active payment currency in July, amounting to 2.04 percent of all payments, up 0.43 percentage points from June. In addition, the value of renminbi payments went up by 9.91 percent, while other payment currencies decreased by 2.5 percent on average month on month. Today's situation differs from the devaluation that took place in 2016 when the yuan's international payment value declined as much as 29.5 percent compared to 2015, closing out the year in sixth place among currencies used for international payments. As far as the internationalization of the yuan is concerned, the impact of this year's exchange rate fluctuations is not as significant as 2016 because it is affected by both external and internal elements. "The internationalization of the renminbi is a convergence of multiple elements, and the exchange rate is just one of them," Sun Jie, a researcher with the Institute of World Economics and Politics under the Chinese Academy of Social Sciences, told Beijing Review.

China launches the first crude oil futures contract at the Shanghai International Energy Exchange on March 26 (XINHUA) Roll booster As an external factor in the progress of the yuan's internationalization, the greenback played a key role this time. "The yuan's internationalization progressing amid depreciation can be attributed to the roll booster: the U.S. dollar," said Marc Chandler, global head of currency strategy with Brown Brothers Harriman, in an interview with 21st Century Business Herald. Chandler explained that as the dollar continues to appreciate and the Federal Reserve (Fed) continues to raise interest rates, dollar-funding costs will spike, forcing more firms to reduce cross-border payments in dollars, which creates room for the yuan's cross-border trade. As of the first quarter, the share occupied by the renminbi in global foreign exchange reserves had increased for three consecutive quarters, accounting for 1.39 percent, a 0.17-percentage-point increase from the end of 2017. In contrast, the share of the dollar dropped from 62.72 percent in the fourth quarter of 2017 to 62.48 percent in the first quarter of 2018, the lowest level since 2013, according to data from the International Monetary Fund. In addition, as of the end of the second quarter, the total financial assets priced in the yuan held by overseas institutions and individuals amounted to 4.9 trillion yuan ($715.7 billion), among which stocks and bonds increased to 2.5 percent and 3.0 percent, respectively, according to data released by the Industrial and Commercial Bank of China Hong Kong, This year, not only China, but the whole world has been shrouded by the shadow of the U.S. trade war. Some emerging markets experienced currency crises as the U.S. dollar remained strong. Many plunged over 10 percent against the dollar. The situation further strengthened the yuan's international usage. To cope with this predicament, countries such as Turkey, Russia and Argentina have signed currency exchange agreements with China and plan to issue renminbi bonds. Meanwhile, the Suez Canal Authority announced on September 9 that it will make the Chinese currency a new form of payment for transit fees in anticipation of the passage of more Chinese ships, while the State Bank of Viet Nam will formally allow the yuan as a payment form in border areas with China starting on October 12, marking the Chinese currency's inclusion in the payment systems of more countries. March 26 is a landmark date for the valuation functions of the yuan as an international currency. It marked the launching of China's first crude oil futures contract in Shanghai, adding a long-awaited Asian benchmark to the global oil sector and stealing market share from the incumbent crude benchmarks of Europe's Brent and the United States' West Texas Intermediate (WTI). In July, Shanghai's crude futures accounted for 14.4 percent of shares, compared with 28.9 percent for Brent and 56.7 percent for WTI, challenging the dominance of Western price-makers.

A Pakistani currency dealer hands over Chinese currency to his customer in Quetta, Pakistan, on January 3 (VCG) Capricious rates To realize the internationalization of the renminbi, it is essential to focus on internal factors as well. Thus, a reasonable exchange rate system is an integral part for the yuan's globalization. The 2018 Q2 China Monetary Policy Implementation Report released by the People's Bank of China (PBC) on August 10 emphasized that China insists on a managed floating exchange rate system with market supply and demand as the basis and in reference to a basket of currencies for adjustment. Both the first quarter appreciation and the second quarter depreciation were driven by market forces, indicating that the central bank has ended normal intervention. At the opening ceremony of the 12th Summer Davos Forum on September 19, Premier Li Keqiang responded to critics who allege that China is manipulating its currency. "The recent fluctuations in the exchange rate have been seen by some as an intentional measure on the part of China. This is simply not true. Instead of engaging in competitive devaluation, China will stick to market-oriented foreign exchange rate reform." "The recent fluctuations are a market-driven result as the Sino-U.S. trade spat affects market expectations," Sun said. Although weakened against the dollar, the renminbi remained strong against a basket of major currencies. According to a research report by China International Trust and Investment Corporation Securities, the first half of the year saw a 0.9-percent appreciation of the renminbi index despite a slight fall since April, suggesting the yuan's stronger resilience against major currencies. The report was based on the China Foreign Exchange Trade System, with the renminbi index used to indicate the effective exchange rate between the yuan and a basket of major currencies. According to the report, the disparity between the depreciation range of the yuan and the dollar and the renminbi's overall exchange rate against the basket of currencies a reflection of its globalization in recent years, making market forces a decisive factor in the Chinese exchange rate system. However, although China ended normal intervention to make the market a decisive force and guaranteed the independence of its monetary policy, it doesn't mean that no further intervention will be exerted to prevent the currency from too sharp a fluctuation. Sun emphasized that in light of the current situation, China should adapt to market variations. However, it is essential to avoid an expectation-driven sharp depreciation, which would result in problems or even risks. In response to the yuan's drastic drop in July, China's central bank took steps in August to steady the currency. But instead of selling billions of dollars to buy yuan as was done in 2016, this time a system of prudent macro-management was adopted, according to the Q2 monetary report. In August, a press release from China's Foreign Exchange Market Self-Discipline Mechanism Secretariat said that the countercyclical factor China reintroduced will play a positive role in keeping the renminbi exchange rate basically stable at an appropriate and balanced level. Meanwhile, on September 20, the PBC announced that it had entered into a memorandum of understanding with the Hong Kong Monetary Authority to facilitate the issuance of Central Government bonds in Hong Kong, which could add to the basket of yuan-denominated financial products with high credit ratings available in Hong Kong. Zhou Hao, a senior Asia economist at the German Commerzbank, said the move at this vital moment was aimed at stabilizing the exchange rate as the Fed is expected to raise interest rates. The issuance will improve the yield curve of renminbi bonds in Hong Kong and support the development of offshore renminbi business in Hong Kong, a positive step for the yuan's global usage. These effective interventions by the PBC to keep the exchange rate within a stable range played a significant role in the yuan's internationalization.

Core engine "In the short run, the volatility of the exchange rate indeed affected the internationalization of the renminbi," Sun said. "Since the exchange rate reform on August 11, 2015, the yuan's internationalization has shown a slight deceleration trend. But the short-term slowdown is conducive to gaining experience, preparation and adjusting policies." "But in the long run, the macro fundamentals are the key element that matters more," said Sun. "As China opens its door wider and international cooperation advances further, China's currency will see wider usage in a global context." The exchange rate system and the macro fundamentals are both internal factors that impact the yuan's globalization. This year, the yuan's good performance on its way toward internationalization was fundamentally boosted by the construction and opening up of the financial market as it became the core engine for the yuan's usage around the world. Patrick Hess, a senior financial market infrastructures (FMIs) specialist with the European Central Bank, suggested that a safe, effective and open construction of FMIs can bolster China's financial market development. This year, the central bank has taken many steps to improve the renminbi cross-border business system including supporting interbank borrowing, cross-border account financing and bond repurchasing in the interbank bond market, which have facilitated renminbi cross-border trade and investment and provided adequate liquidity for the development of offshore yuan business. Moreover, Yi Gang, PBC Governor, said on September 18 that China will further open up its financial market by easing restrictions on foreign equity, forms of establishment and the qualification of foreign shareholders of financial institutions, which will help to attract more foreign investment in Chinese bonds and stocks, guiding the renminbi to become a new reserve currency and vitalizing its usage. Hess thought the improvement of FMIs could boost the Chinese currency's investing and reserving functions and help to better serve the projects in nations along the Belt and Road. According to the Bank of China Beijing Branch, the total volume of payments between Beijing and Belt and Road countries reached 202.8 billion yuan ($29.6 billion) in the first half of 2018, an 84.6-percent increase year on year. "To promote the yuan's globalization, from a more farsighted perspective, it is important to highlight the overall performance of the economy by scaling up the economy and trade, managing inflation well, stabilizing the financial market to prevent it from speculative fluctuations and more importantly, making it more open to the world," Sun concluded. Copyedited by Rebeca Toledo Comments to zhangshsh@bjreview.com |

|

||||||||||||||||||||||||||||

|