|

| Business |

| Freeing Reserve Cash | |

| China further cuts the reserve requirement ratio for banks to boost the real economy | |

|

|

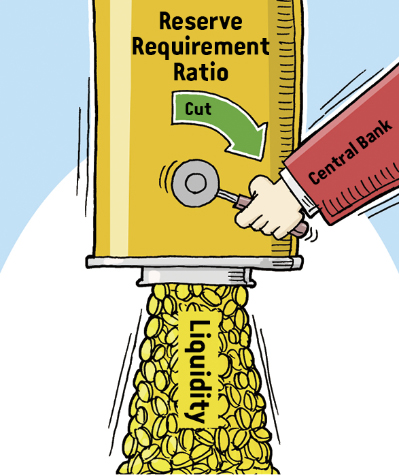

The People's Bank of China lowers the reserve requirement ratio for most banks by 1 percentage point on October 15 (VCG)

On October 15, the reserve requirement ratio (RRR) for most banks in China went down by 1 percentage point, the fourth such cut in 2018. The People's Bank of China (PBC), the country's central bank, announced the decision on October 7, saying the measure is mainly aimed at optimizing the structure of liquidity in commercial banks and the financial market so that the financial sector can better serve the real economy.

Some of the liquidity unleashed by the reduction was used to pay back 450 billion yuan ($65.22 billion) of medium-term lending facility (MLF) due on October 15. In addition, the RRR cut also released another 750 billion yuan ($108.7 billion) of incremental capital, according to PBC statistics. The cut applied to the renminbi deposits of large commercial banks, joint-stock commercial banks, city commercial banks, non-county rural commercial banks as well as foreign-funded banks. Serving real economy better As more credit is granted, financial institutions' demand for medium- and long-term liquidity is also increasing. Moderately cutting the reserve requirement, the amount of deposits that a bank must keep on hand at all times, has stabilized funds within the banking system. Besides improving the liquidity structure in commercial banks and the financial market, it will also allow financial institutions to access long-term funds steadily and subsequently reduce corporations' financing costs. The 750-billion-yuan incremental capital to be freed will enable financial institutions to better support small and micro-sized enterprises, private companies and innovation-driven firms. All this will enhance the innovative vigor and resilience of the economy and boost sound development of the real economy, said a PBC statement on the RRR cut. "This time of RRR reduction conforms to the changes in the Chinese economy," Lian Ping, chief economist of Bank of Communications, one of China's largest commercial banks, said in an interview with China National Radio. According to him, China's prudent monetary policy remains neutral, and the adjustments target specific circumstances. In the banking system, growth of debts has been slow for some time, and compared with the increase of loans, that of deposits has been slower. The market demand for liquidity has been growing steadily. Considering the debt changes in the banking system and the fact that the RRR is still at a comparatively high level, making appropriate adjustments is a targeted policy that can help commercial banks better support small and micro-sized businesses, private companies and innovation-driven firms. This was the second time that the central bank cut RRR to replace MLF operation this year. "This will expand the maturity structure of funds, ultimately helping improve financing conditions of corporations," said Lu Zhengwei, chief economist of Industrial Bank, in an interview with China National Radio. Lu said previously both open market operations and MLF matured within one year, but this RRR cut unleashed long-term capitals, which would make the maturity of assets and debts in commercial banks better matched. "This would encourage commercial banks to grant more loans and buy more medium- and long-term corporate bonds, which would improve the financing conditions of private enterprises," he added.

Monetary policy unchanged According to the PBC statement, the RRR cut is still a measure of targeted control, with liquidity in the banking system as well as money supply staying stable and the orientation of monetary policy remaining unchanged. Some of the liquidity released by the RRR cut was used to pay back MLF, which is a kind of replacement of two liquidity tools. Therefore while the liquidity structure is optimized, the total amount of liquidity in the banking system remains unchanged. "The PBC will continue the prudent and neutral monetary policy, refrain from using a deluge of stimulus and focus on targeted control, in order to maintain sound and sufficient liquidity," according to the statement. The policy is also intended to promote reasonable growth of monetary credit and the total financing amount. In addition, it will create a "suitable monetary and financial environment for quality development and supply-side structural reform." Will the RRR reduction intensify the depreciation pressure on the renminbi? The PBC said as the interest rate remains stable and the growth of broad money [that covers cash in circulation and all deposits] and total financing amount is suited to the nominal GDP growth, the RRR reduction will not impose depreciation pressure on the renminbi. Instead, it will facilitate economic restructuring, boost high-quality development and make economic conditions better support the renminbi exchange rate. As a large developing economy, China is very competitive in exports and its economic growth mainly relies on domestic demand with complete categories of manufacturing industries and a well-developed industrial system, the statement added. There are sufficient conditions for the renminbi exchange rate to remain basically stable. The PBC will continue to take necessary measures to stabilize market expectations and keep the foreign exchange market running smoothly, it said. However, Zhang Ming, a researcher with the Chinese Academy of Social Sciences and chief economist of Ping An Securities, told Economic Information Daily that given the backdrop of several interest rate hikes by the U.S. Federal Reserve, the RRR cut will help narrow the interest rate spread between China and the United States, bringing depreciation pressure to the renminbi against the U.S. dollar. Zhang added that the PBC statement shows the central bank is putting domestic targets before foreign-related targets, and is willing and able to keep the renminbi exchange rate at a certain level. "New counter-cyclical factors have enabled the central bank to better influence the yuan's standard price," Zhang said, adding with enhanced administration of cross-border capital flows, the PBC still has the ability to intervene in foreign exchange reserves and the offshore renminbi market. Copyedited by Sudeshna Sarkar Comments to wangjun@bjreview.com |

|

||||||||||||||||||||||||||||

|