|

| Opinion |

| Household Debt Deleveraging Should Be Accelerated | |

| China should take measures to control rising household debts | |

|

|

|

(XINHUA)

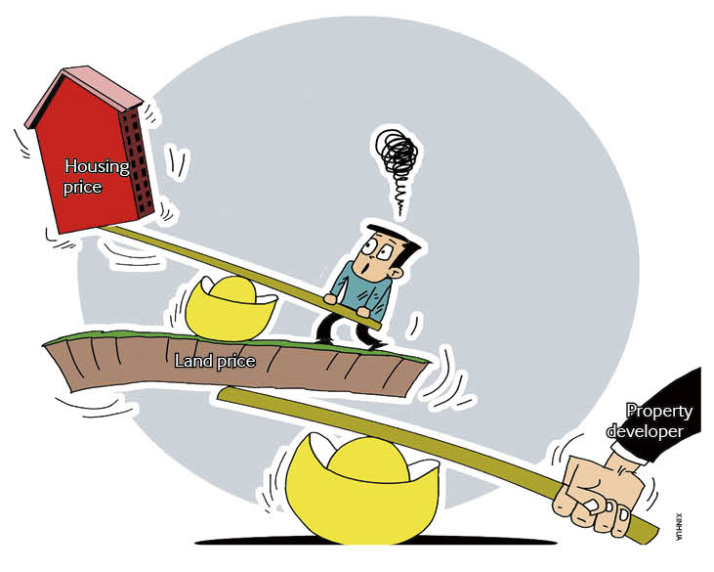

A report recently released by the Research Institute of the Shanghai University of Finance and Economics (SUFE) showed that China's household debt is growing rapidly. By the end of 2017, the ratio of China's household debt to disposable income had reached 107.2 percent, higher than that in the United States and approaching the U.S. peak level before the outbreak of the financial crisis of 2008. The report said that authorities should pay more attention to the problem of high household debt and regard household deleveraging as important as the deleveraging of corporates and local governments so as to push relevant efforts ahead with practical results and ensure the economy performs in a balanced manner. In other words, China's deleveraging drive may falter if the focus is limited to corporates and local governments. The reasons leading to China's high household borrowing are multiple. First of all, relevant analyses show that a key factor lies in the surge of housing prices aside from the rise of debt burden caused by increasing household expenditures on education, medical care and elderly care. More than 70 percent of Chinese households are property owners and many of their houses are bought through mortgage loans, funds from other financing institution or money borrowed from relatives and friends. Another important reason is that the performance of many small private enterprises is not promising, especially in coastal regions in southeast China where the private economy thrives. By the end of 2017, the ratio of household debt to disposable income in more than 10 provinces and municipalities exceeded 100 percent. The ratios in Fujian, Guangdong and Zhejiang provinces have surpassed the peak value of the U.S. debt-to-income ratio before the financial crisis of 2008, with Beijing also approaching this high level. That is to say, household debt is higher in regions with better developed economies and more private enterprises. A high household debt ratio will not only hinder the improvement of residential consumption capability and quality but also stand in the way of the deleveraging of local governments. The high leverage of corporates and households may even block the deleveraging of the financial sector and expose banks to greater operational risks. The tightening of household liquidity is likely to drag on the vitality of corporate operations and eventually affect banks, threatening the stability of the whole financial system. Research by SUFE shows that an increase of 1 percentage point on the amount of non-performing loans from commercial banks will decrease the annual GDP growth rate by 1.5 percentage points. Therefore, comprehensive policies should be adopted to reduce the household debt ratio. Reform of the income distribution system should be deepened so as to ensure the growth of residential income surpasses that of the GDP and households' capacity to reduce debt leverage should be improved. The government also needs to reform personal income tax policies and further lower taxes for individuals and households. The rise of housing prices should also be curbed to ensure the sound development of the real estate market. Last but not least, China should improve its social security system and provide more public services and support for elderly care, medical care and education to ease people's concerns. This is an edited excerpt of an article written by Mo Kaiwei, a researcher with the Chinese Academy of Regional Finance, and published in National Business Daily Copyedited by Rebeca Toledo Comments to zhouxiaoyan@bjreview.com |

|

||||||||||||||||||||||||||||

|